It’s tempting to take advantage of the mortgage deferrals available from Canada’s major banks during the pandemic, however it’s important to take a moment to consider if it’s the best option for your situation.

It is also important to know that mortgage payment deferrals are not financed by a government program. The financial burden falls on the mortgage lenders. Banks and non-bank lenders alike, fund mortgages with other debt, including covered bonds, deposit notes, commercial paper and mortgage backed securities. The monthly interest and in some cases principal on these debt instruments, must still be paid even while the payments on underlying mortgages are deferred.

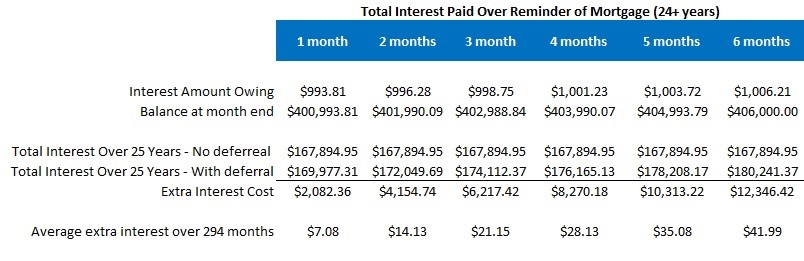

Nearly 600,000 Canadians have so far taken advantage of some form of mortgage deferral assistance, due to the COVID-19 crisis, according to the Canadian Bankers Association (CBC). Of course, taking advantage of mortgage payment deferrals, naturally comes at a cost as mentioned and that has been calculated at up to $12,000 in extra interest costs for those taking the full six-month deferral.

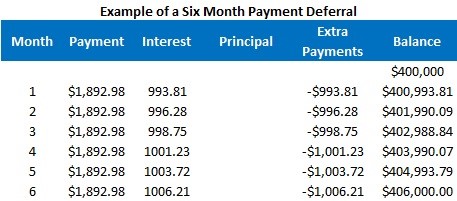

Mortgage deferral costs for someone with a mortgage rate of 3% and amortized over 25 years (and assuming they just bought a house and immediately deferred payments), would amount to $2,082 in additional interest for a one-month deferral, $6,217 for six months and $12,346 for a six-month deferral, when added back into the life of the mortgage and assuming no extra repayments.

Original Article: www.canadianmortgagetrends.com